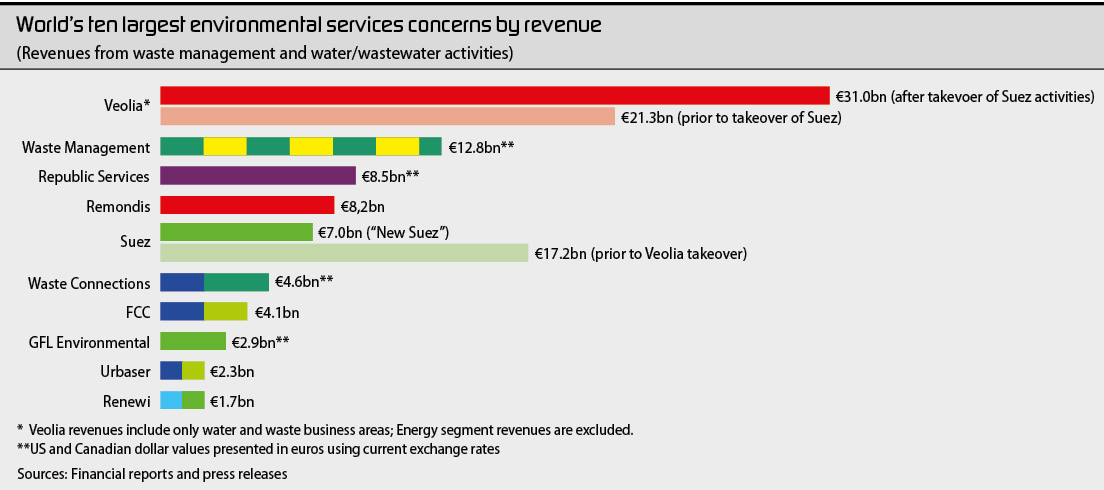

In seeking to acquire competitor Suez, Veolia CEO Antoine Frérot said he aimed to create a "world leader of the ecological transformation". A review of the annual revenue figures of the industry’s major players reveals that the partial merger now expected to close late this year will only widen the gap between Veolia and its next largest competitor. The integration of the Suez activities earmarked for takeover would bring Veolia’s new consolidated revenues to around €37bn per year. Of that total, some €31bn would be generated by the concern’s waste and water activities, while the remainder would stem from the energy segment.

Following the sale of Suez, the world’s second and third largest environmental services companies will be the two US waste management companies Waste Management and Republic Services. However, both of these groups are active only in North America. Both Veolia and the fourth-ranked Remondis are active in markets on several continents.

Remondis, Germany’s largest environmental services group currently generates annual revenues of around €8.2bn. It’s no secret that the concern, with its long history of acquisitions is keen to continue expanding. Remondis had sought to acquire a stake in the pared-down, post-merger Suez. In its formal offer, the waste management company stated that it would like to purchase 20 per cent of the "new Suez", but at the same time was prepared to increase its share to up to 40 percent of the new entity’s capital. Remondis CEO Ludger Rethmann emphasized in his offer letter to Suez’s top management that his concern would not require any external financing to complete the transaction. In the end, however Suez and Veolia agreed on a sale to a consortium consisting of Meridiam, Global Infrastructure Partners (GIP) Caisse des Dépôts Group and the insurance company CNP Assurances.

Rapid expansion at Paprec and Prezero may

make them near-term additions to the top ten

This spring Jean-Luc Petithuguenin, founder and CEO of the French recycling group Paprec, had also expressed interest in acquiring some of Suez’ waste activities were they to be sold off. Paprec, which has its institutional roots in the French paper recycling segment, has been increasingly expanding into the waste management sector, and recently into the energy from waste (EfW) sector. Following the planned takeovers of CNIM’s waste to energy operation and management O&M activities and of Dalkia Wastenergy, Paprec aims to generate €2bn in revenues in the current business year, which would easily put it striking distance of a spot in the top ten. Paprec was also considering other takeovers, and was named earlier this year by Spanish media among the potential buyers for the Cespa, the waste management subsidiary of the Spanish conglomerate Ferrovial. Other interested parties were said to include Remondis, but also Lidl parent company Schwarz Group.

Schwarz’s environmental services subsidiary, Prezero will be another company to watch in the near term. The company has been on a rapid expansion course in recent years, acquiring the activities of Tönsmeier, then Germany’s fifth largest waste management company with revenues of €500m. Last year, it purchased Suez’s Swedish activities, with their annual revenues of around €250m. And the European Commission recently gave the green light for Prezero to acquire the majority of Suez’s waste management activities in Germany, the Netherlands, Luxemburg and Poland, which will put another €1.1bn in annual sales revenues in Prezero’s column.

FCC, Urbaser and Renewi remaining

European concerns in the top ten

Trailing Suez in the list of top 10 environmental services groups are the North American concerns Waste Connections and GFL Environmental, which like their competitors Waste Management und Republic Services are active almost exclusively in the US and Canada. The Spanish concerns FCC and Urbaser and the Dutch-British waste management company Renewi round out the top ten. Both FCC and Urbaser are active outside of Europe, while Renewi divested its Canadian assets in 2019. Currently, the company is active only in the EU and UK.

No Chinese firms in the top ten (yet)

Chinese environmental services groups are not in the same league as the largest European and North American players – at least not yet. However, in the midst of its bid for Suez, Veolia repeatedly raised the spectre of future takeovers by Chinese investors, concerns echoed by Remondis. And Chinese investors have been active on the European waste management and recycling market for years. The Deng family has holdings in the Alba Group, while the Chiho Environmental Group (2020 revenue, ca. €1.45bn) owns scrap recycler Scholz. China Tianying only recently reached an agreement to sell Spanish services company Urbaser to US investor Platinum Equity. In the wte segment, Li Ka-shing’s CK Infrastructure (CKI) took over the Dutch EfW plant operator waste AVR in 2013, and Beijing Enterprises Holdings Limited holds Germany’s largest EfW company EEW. Still none has yet reached the scale of the world market leaders.

")